Clarifying reporting about Loan Level Price Adjustments

There have been numerous reports in the media recently about rate/loan fee adjustments that took effect on May 1, 2023. As with any hot topic, some of the reports are full of accurate information and paint an unbiased picture for the reader while others contain some accurate information mixed with a biased slant to move the reader to the position that the writer has adopted.

To be fair, the topic is complex, and it is understandable that some of the nuances can be missed if you have not spent years working in the mortgage industry. To learn more about the upcoming changes to Loan Level Price Adjustments (LLPA’s) through an unbiased lens and better understand the real impact on first time homebuyers, continue reading this overview.

What is a Loan Level Price Adjustment (LLPA)?

LLPA’s are fees imposed by Fannie Mae and Freddie Mac, the two entities that guaranty the majority of newly originated mortgages. The fees are based on loan features such as credit score, the loan-to-value ratio, occupancy (owner vs. non-owner-occupied homes), and soon, your debt-to-income ratio. LLPA’s can show up in either the up-front fees (closing costs) or interest rate charged to the borrower.

Who made the change?

The Federal Housing Finance Agency (FHFA) was established by the Housing and Economic Recovery Act of 2008 (HERA) and is responsible for the effective supervision, regulation, and housing mission oversight of the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), and the Federal Home Loan Bank System, which includes the 11 Federal Home Loan Banks (FHLBanks) and the Office of Finance (OF). The Agency’s mission is to ensure that Fannie Mae and Freddie Mac (the Enterprises) and the FHLBanks (together, “the regulated entities”) fulfill their mission by operating in a safe and sound manner to serve as a reliable source of liquidity and funding for housing finance and community investment. Since 2008, FHFA also has served as conservator of Fannie Mae and Freddie Mac.

On January 19, 2023, the FHFA announced changes to single-family pricing structure (LLPA’s) effective May 1, 2023. You may read the press release here. You can also follow this link to see the new LLPA Matrix.

Whom does it impact?

Anyone taking out a mortgage guaranteed by Fannie Mae and Freddie Mac, which is the majority of mortgages originated. You will often hear these loans referred to as “conventional” loans.

There are many first-time homebuyer mortgage loans that are not guaranteed by Fannie Mae or Freddie Mac and are, therefore, not the subject of the LLPA changes. Examples of loans not included in the LLPA changes include FHA loans, VA loans or special first-time homebuyer portfolio loans offered by banks, credit unions or organizations like INHP. In fact, most clients that come to INHP end up choosing either a bank portfolio product, an FHA loan or an INHP loan.

What is all the chatter about?

The new LLPAs that took effect May 1 featured a reduction in the LLPA fees charged for loans to borrowers with lower credit score and lower down payment amounts. Some higher credit score and higher down payment loans will also see a reduction in LLPA fees while others may see a slight increase. This has caused some critics to suggest that first-time homebuyers with lower credit scores and lower down payments (less than 20% of the home’s value – often referred to as a high loan-to-value or high LTV loan) will pay less than homebuyers with higher credit scores and higher down payments (20% or more of the home’s value). The observation is that a borrower with a lower credit score and higher LTV is a higher credit risk and should have fees commensurate with the risk level. Conversely, a borrower with a higher credit score and lower LTV is a lower credit risk and should have fees commensurate with the reduced risk level.

What often gets missed in this line of discussion, however, is that a borrower that contributes less than 20% of the homes value via down payment, will also have additional fees added to the total cost of their loan through private mortgage insurance (PMI) which reduces the loan risk level for Fannie Mae and Freddie Mac and increases the total fees or cost of the loan to the borrower. When the additional cost of PMI is taken into consideration, the total fees associated with a loan to a lower credit score and higher LTV borrower are indeed higher than those associated with a loan to a higher credit score and lower LTV borrower. Lower credit score borrowers with a higher LTV loan will be paying more in total fees for the corresponding increased risk level.

Are there other misconceptions to consider?

Various media reports also have led some to believe that it would be a rational decision for prospective first-time homebuyers with lower credit scores and lower down payment amounts to forego any efforts to increase their credit score or save for additional down payment towards the purchase of a home. Although this may be the takeaway for some, or even many prospective first-time homebuyers, it would be a shortsighted and misinformed decision.

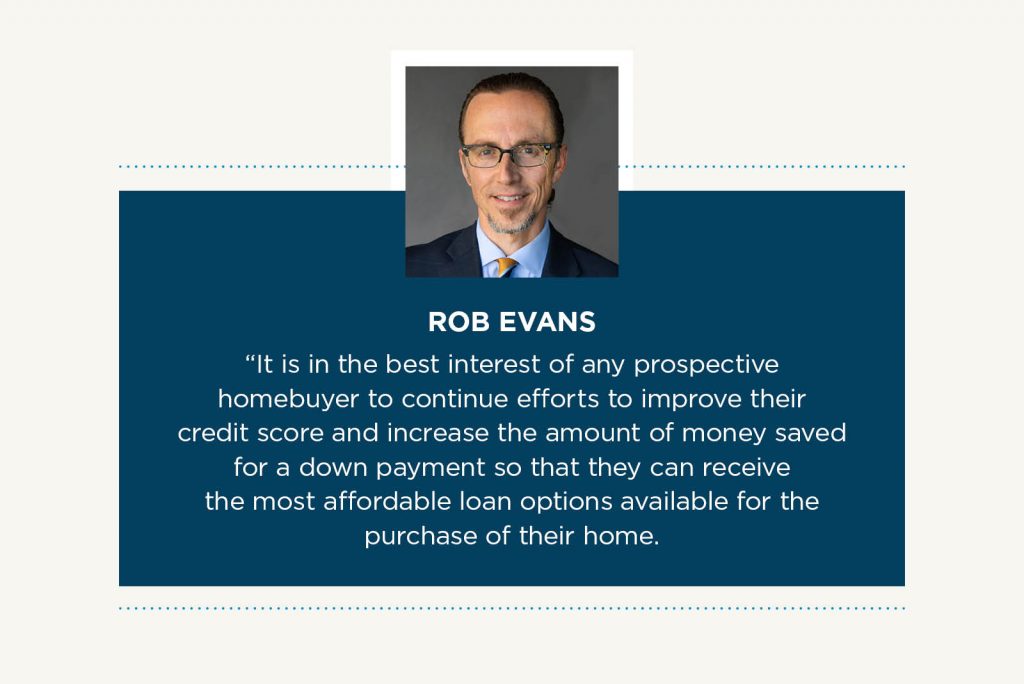

While it is true that the LLPA fees associated with a lower credit score higher LTV loan have been reduced and will result in a more affordable loan option for the borrower, the lowest LLPA fees and best rates continue to be realized by borrowers with a higher credit score and lower LTV. Even with the reduction in LLPA fees associated with a lower credit score and higher LTV loan, such loans will continue to have higher fees (whether it is through up-front fees, higher interest rate or both) than a loan featuring higher credit scores and a lower LTV. And the addition of fees associated with PMI will continue to make this a costlier loan than one to a higher credit score borrower with a larger down payment. It is in the best interest of any prospective homebuyer to continue efforts to improve their credit score and increase the amount of money saved for a down payment so that they can receive the most affordable loan options available for the purchase of their home.

INHP’s response?

It is a complex topic to be sure, and there are many other parts of the LLPA changes that we could explore. For our part, INHPs focus continues to be on the impact of this change to the first-time homebuyers that we serve. We will continue our efforts to empower clients to be knowledgeable consumers with skills necessary to make informed choices and be successful in the mortgage and home buying market.

Rob Evans

Executive Vice President, Government and Community Affairs

###