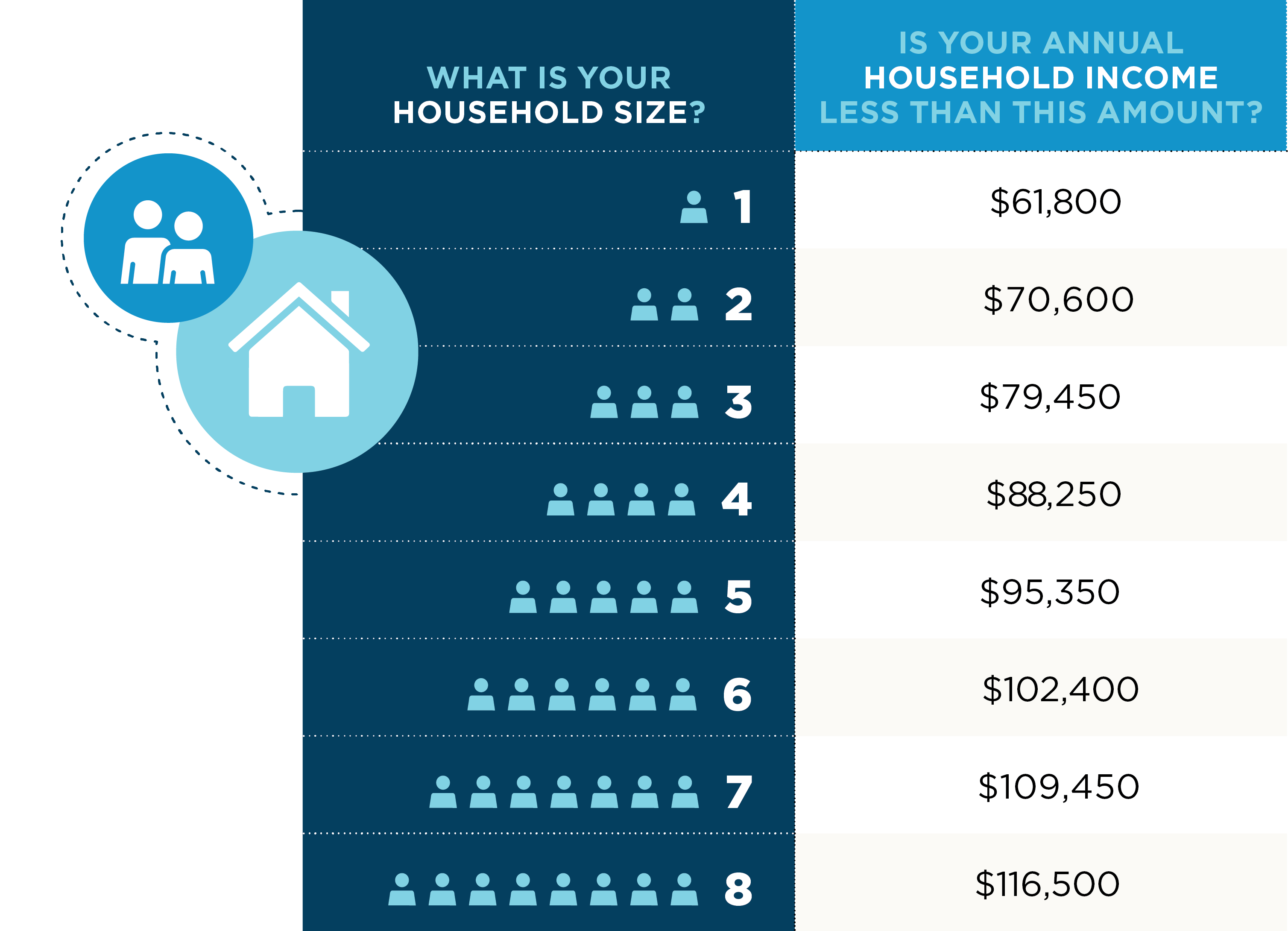

What “no money down” means

Question: Does a mortgage loan offering “no money down” mean you can buy a home without having any money saved? Answer: No – there are other costs you should be prepared to pay during the homebuying process. But, a no money down (also called zero money down) loan offer can reduce those up-front costs significantly and make first-time homeownership easier to reach.

No money down = No down payment

A mortgage loan offering no money down allows the buyer to officially purchase a home without making a down payment – the initial out-of-pocket money needed to take legal homeownership. For example, if a lender requires a down payment of 3% of a $200,000 home, the buyer would need to pay $6,000 as part of the closing transaction. But with no money down, the buyer does not need to have this sum of money at closing, since it is factored into the home loan amount.

On one side, having a down payment at closing will reduce the total loan amount. However, not having to save $6,000 for a downpayment could mean reaching homeownership faster and being able to use that money for home improvements, emergencies, etc. instead.

Other homebuying expenses

Even with no down payment, there are still other homebuying fees to save for – like insurance and closing costs, a home inspection, and appraisal fees. These costs vary, but an unbiased INHP advisor can help you prepare. You may even qualify for an INHP Individual Development Account (IDA) – a special benefit offering a matched-savings account – to help you save money faster to cover those fees.

As with any loan, it’s important to read and understand the terms before signing, including language about no money down offers. Luckily, INHP is here to help if you’re ready to take the next step!