Two ways mortgage lenders view student loan debt

Are you paying off student loans and looking to buy a home?

Here are the two ways mortgage lenders view student loan debt repayment and how each impact how much you can afford:

- Income based repayment: Income based repayment (IBR) is calculated based on your income and family size. It could be calculated to as little as $0 per month to as much as 15 percent of your income. If a mortgage lender uses your IBR when calculating your monthly debt, you may appear to have less monthly debt than you actually have, qualifying you for more of a home loan amount than you can comfortably afford.

- The “1%” rule: This method is often used when you receive a deferment or forbearance allowing you to temporarily stop making student loan payments. The 1% rule, projects your monthly student loan payment to be equal to 1%of the total balance for all your student loans. If a mortgage lender uses the “1%” rule, you may appear to have more monthly debt than you actually have, so a lender may qualify you for less of a home loan amount than you can comfortably afford.

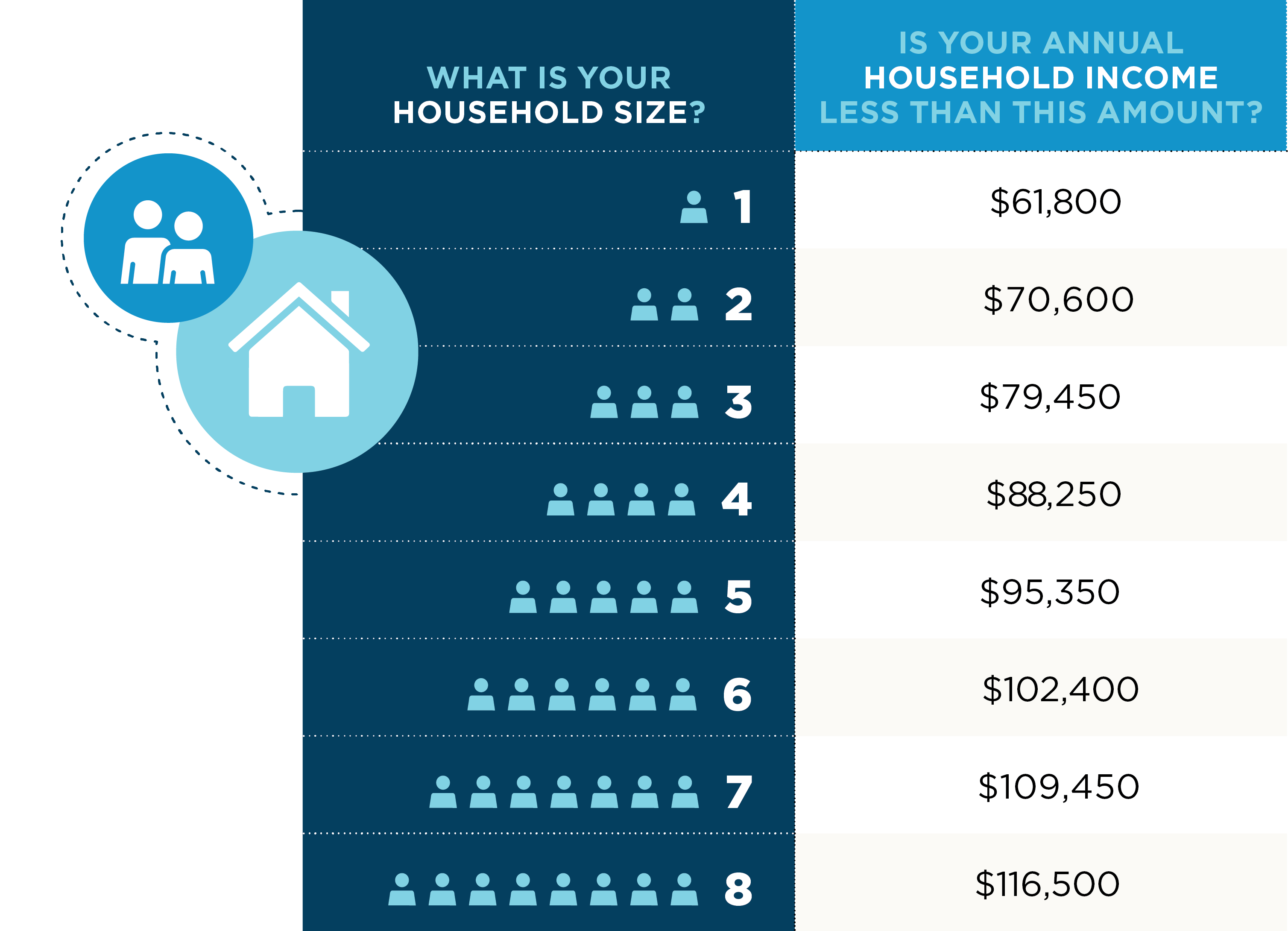

Want to see these concepts as an infographic or need more information? Check out this downloadable resource or talk with the unbiased, trusted experts at INHP about your situation.